Plan 2 vs Plan 5: Which is Cheaper? Income Decides Everything

The post-2023 Plan 5 seems to have lower rates, but the 40-year term could cost low-to-middle earners tens of thousands more. Data shows you which to choose.

Plan 5 launched in 2023 with lower interest (RPI only) but extended repayment to 40 years. This seemingly small change could create a £30,000+ lifetime cost difference. The key is your lifetime earnings trajectory.

Core Differences

| Feature | Plan 2 | Plan 5 | Impact |

|---|---|---|---|

| Repayment Threshold | £27,295/year | £25,000/year | Plan 5 lower, more people pay |

| Interest Rate | RPI + up to 3% | RPI only | Plan 5 is 2-3% lower |

| Write-Off Period | 30 years | 40 years | Plan 5 adds 10 years |

| Monthly Rate | 9% | 9% | Same |

Three Income Scenarios

Using a typical £45,000 loan balance, we model different career paths:

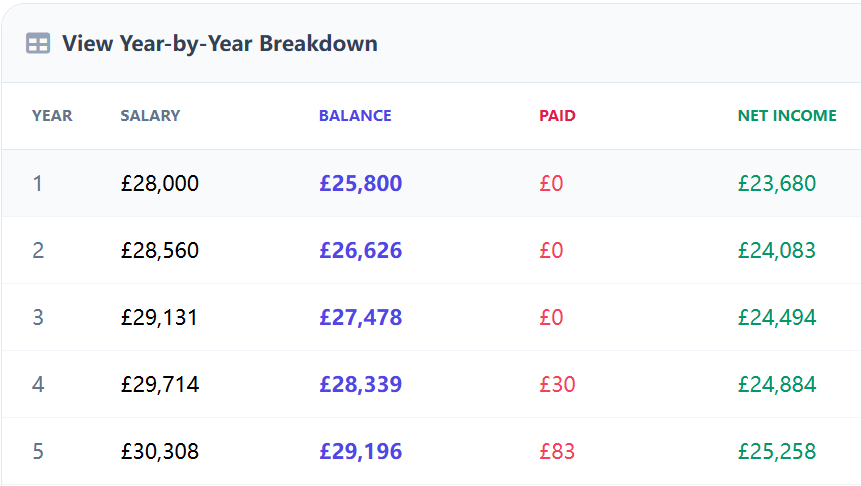

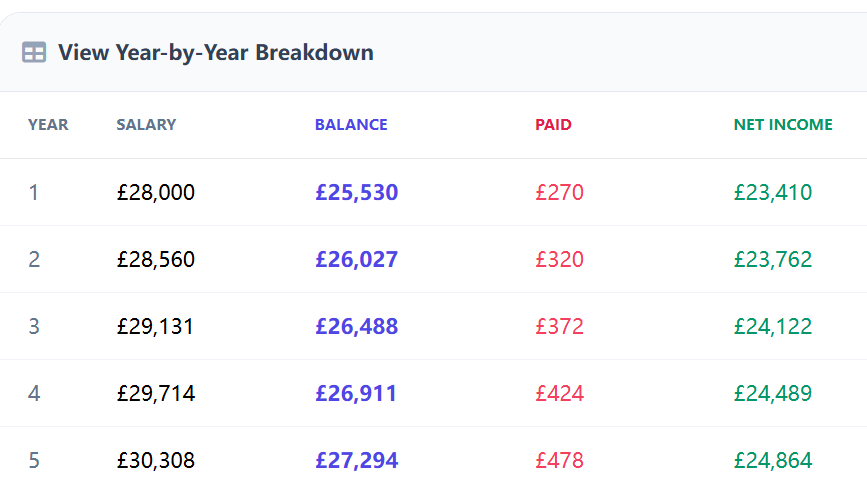

Scenario A: Low Growth (Civil Servant/Teacher)

Starting salary £28,000, 2% annual growth, Loan £25,000

Plan 2 outcome:

• Total repaid: £23,114

• Written off: £51,968

• Effective rate: near-zero

Plan 5 outcome:

• Total repaid: £48,000

• Written off: £32,000

• Effective rate: near-zero but higher than plan2

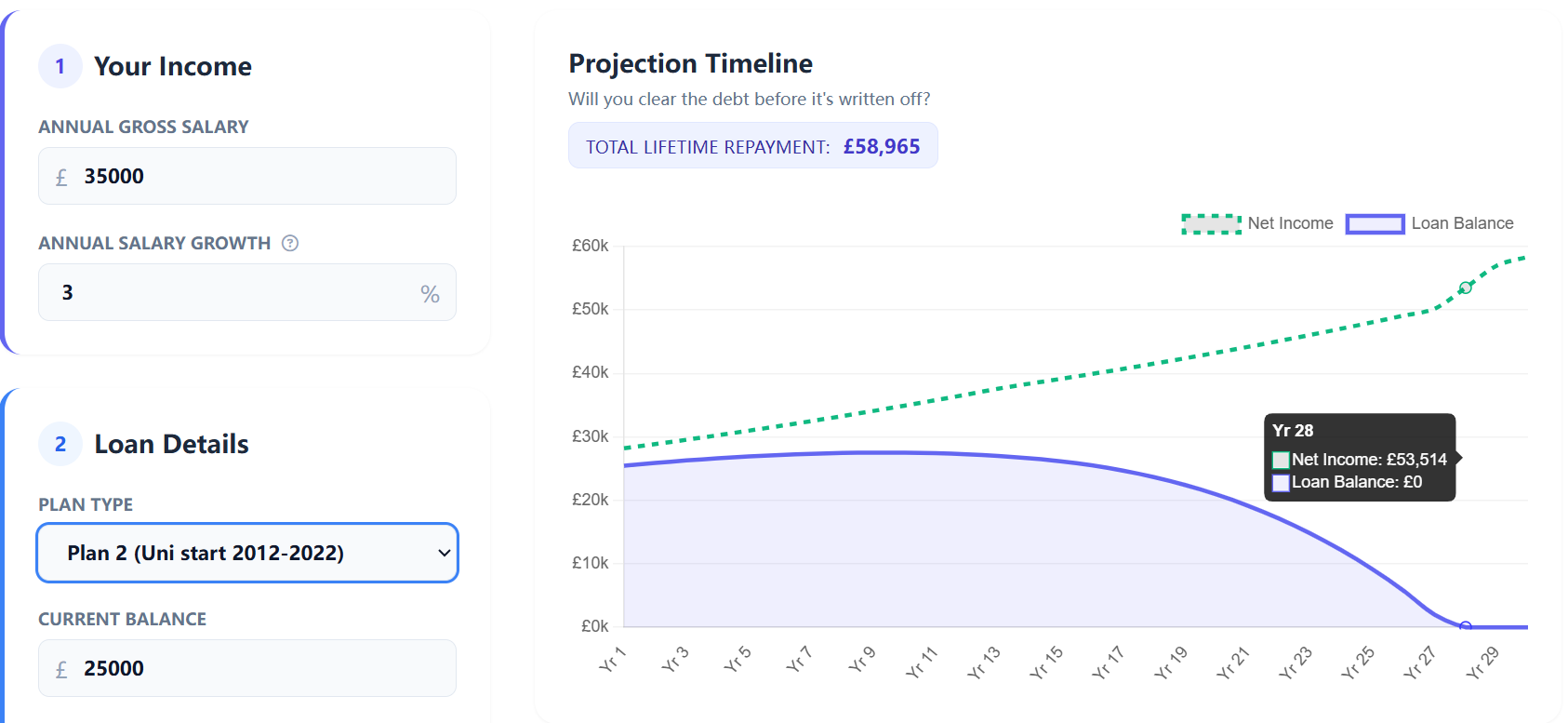

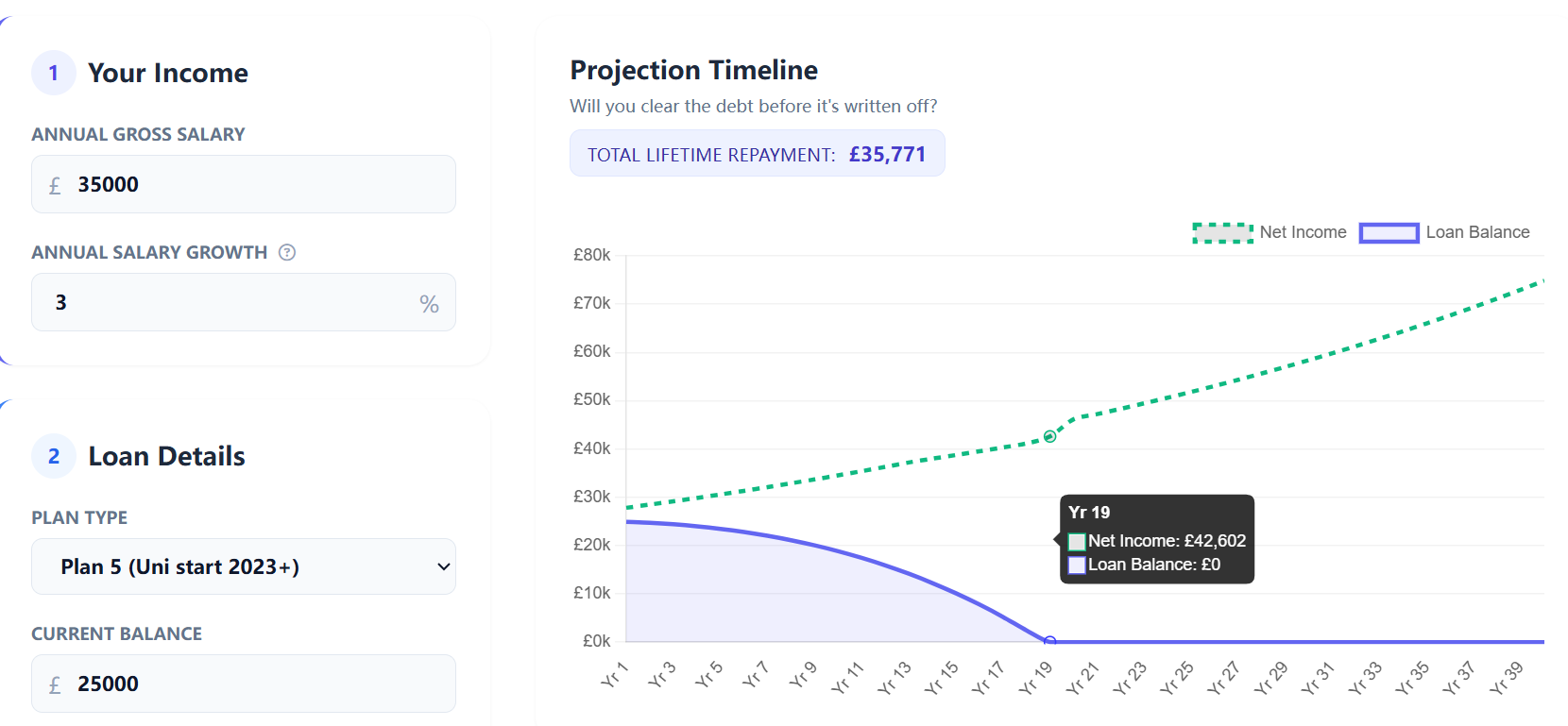

Scenario B: Medium Growth (Engineer/Nurse)

Starting salary £35,000, 3% annual growth, Loan £25,000

Plan 2 outcome:

• Total repaid: £58,965

• Cleared in: 28 years

• Interest paid: £33,965

Plan 5 outcome:

• Total repaid: £35,771

• Cleared in: 19 years

• Interest paid: £10,771

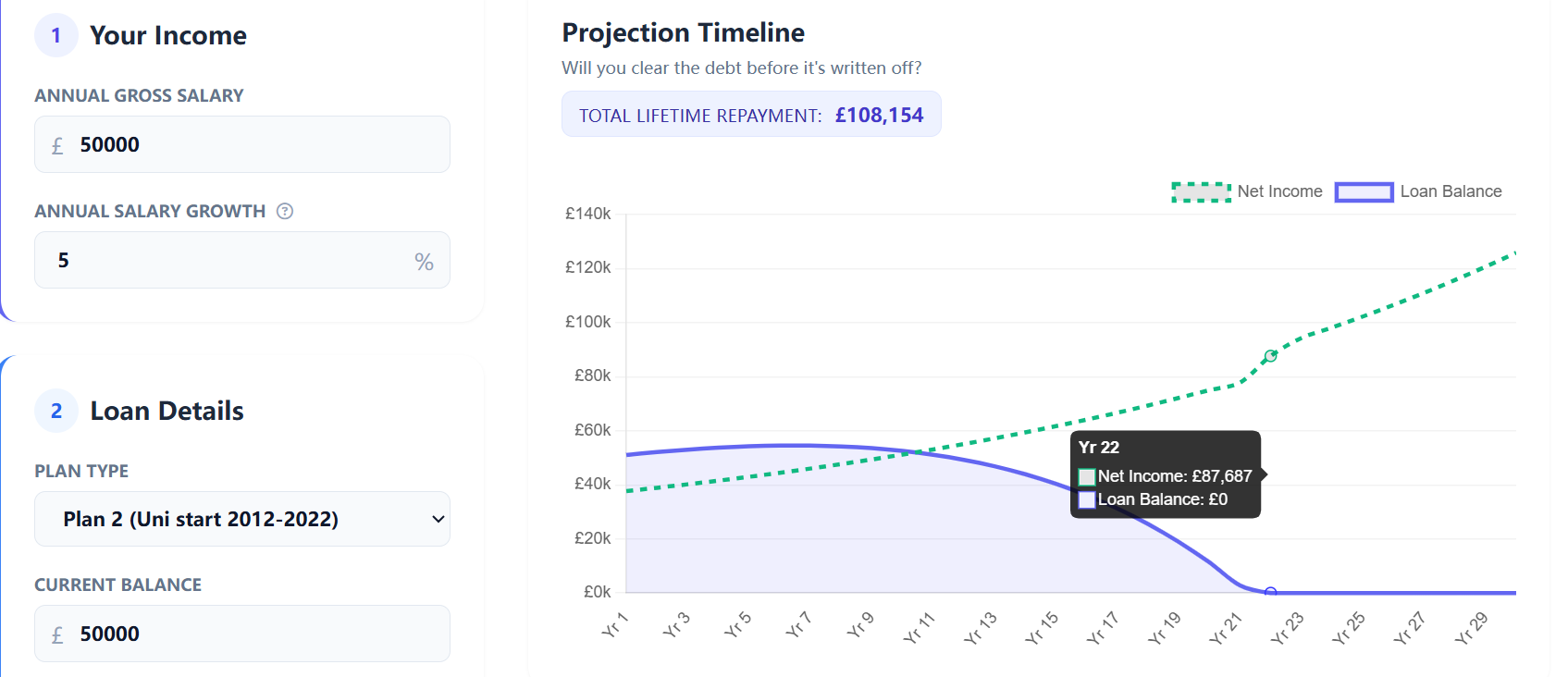

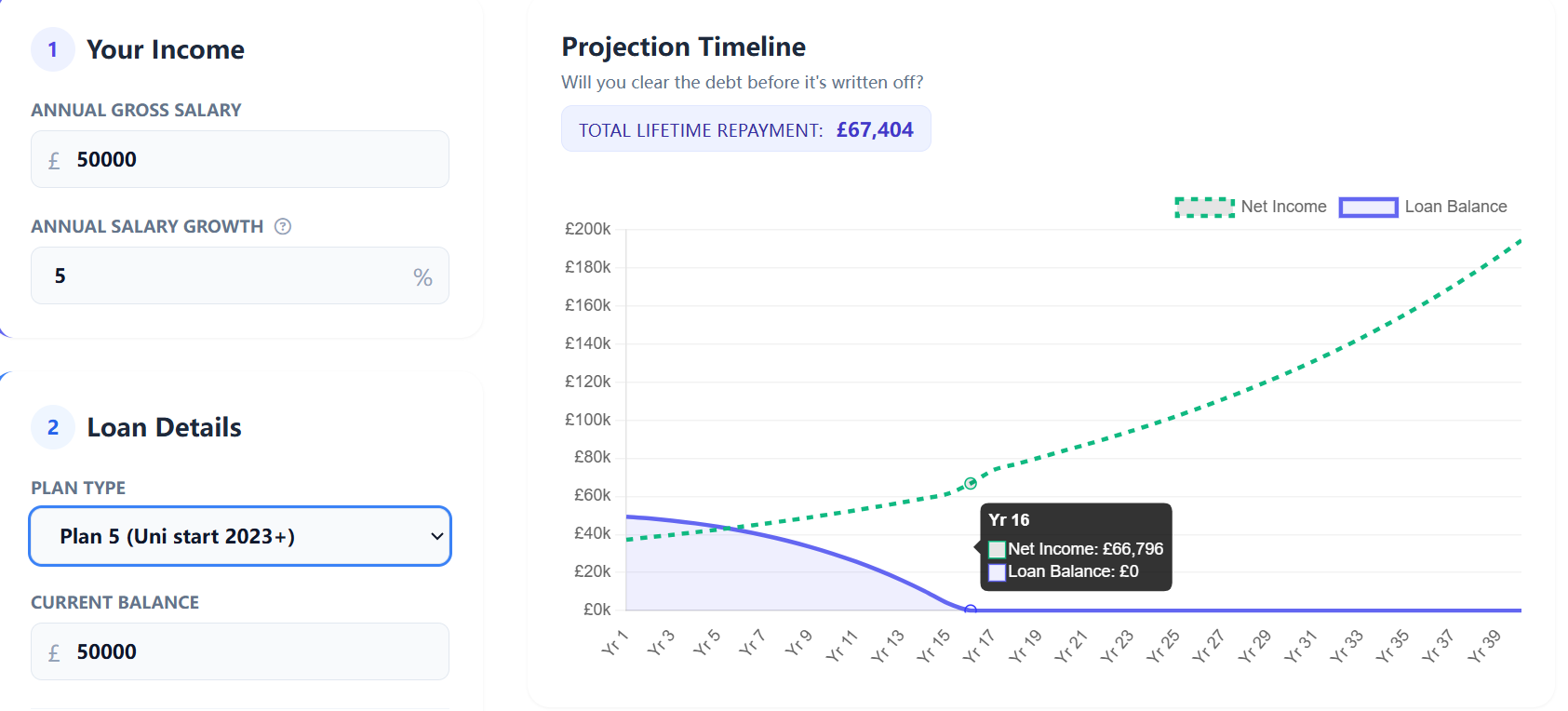

Scenario C: High Growth (Finance/Lawyer)

Starting salary £50,000, 5% annual growth, Loan £50,000

Plan 2 outcome:

• Total repaid: £108,154

• Cleared in: 22 years

• Interest paid: £58,154

Plan 5 outcome:

• Total repaid: £67,404

• Cleared in: 16 years

• Interest paid: £17,404

Key Insight

Plan 5's lower rate seems attractive, but the 40-year term means low-middle earners may pay £15,000-25,000 more before write-off. This is essentially a stealth government revenue increase.

Plan Comparison FAQ

Can I choose between Plan 2 and Plan 5?

Can Plan 5's rate advantage offset 10 extra years?

If I expect big income growth, is Plan 5 better?

Do postgraduate loans also have 40-year terms?

Related Guides

Understanding interest calculation for decision-making

85% of borrowers should NOT overpay