UK Student Loan Interest Rates Explained: RPI, CPI & Plan Differences

Understanding how interest is set is key to mastering your student loan. This guide breaks down RPI, Plan 2 vs Plan 5, and the real 30-year impact of interest.

UK student loan interest rates aren't fixed—they're linked to inflation (RPI). This means your loan can "grow itself." The interest rules vary dramatically between plans (Plan 1/2/4/5), and understanding these differences could save you thousands.

How Interest is Set: RPI & Government Intervention

The core of UK student loan interest is the Retail Prices Index (RPI), a measure of inflation. Every September, the government sets new rates based on the previous March's RPI figure.

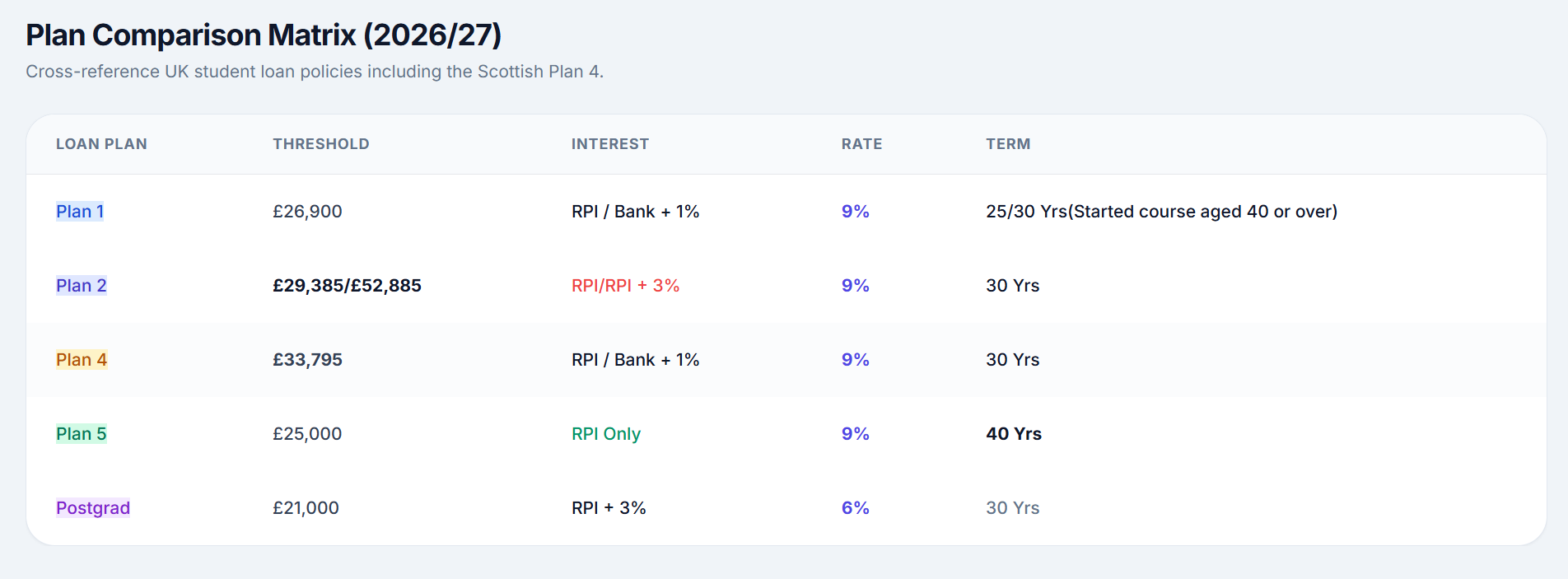

2026/27 Interest Rates by Plan

Plan 2 (2012-2023 starters)

Interest = RPI (3.2%) + up to 3% = 6.2%.

Plan 5 (Post-2023 starters)

Interest = RPI only (3.2%), with no income-based uplift. Significantly lower than Plan 2.

Plan 1 (Pre-2012)

Interest = lower of RPI or Bank Rate + 1%. Currently ~3.2%

Plan 4 (Scotland)

Same as Plan 1: lower of RPI or Bank Rate + 1%. A Scottish student advantage.

Real Impact of Interest: Compound Mechanism

The scary part of student loans is compound interest—interest on interest. If your monthly repayment is less than the monthly interest, your balance grows even while you pay.

Key point: Over 85% of borrowers never repay enough to cover interest, eventually relying on write-off. This means nominal interest is meaningless for most—only high earners and fast repayers need to care.

Future Rate Predictions & Modelling Tips

While 30-year rates can't be predicted accurately, sensible modelling helps you make informed decisions:

- Use Conservative Inflation Assumptions: Model RPI at 3-4% long-term average, not current spikes

- Project Salary Growth: Include realistic promotions and potential career breaks

- Compare Investment Returns: FTSE historical returns ~7-8%, exceeding student loan effective rates

- Calculate Breakeven Point: Find the income needed to start repaying principal

Interest Special Cases & Policy Risks

In 2023, the government first intervened, cutting Plan 2 rates from 12% to 7.3%, showing policy can change. But note:

- Policy changes usually only affect new borrowers: Existing loan terms typically remain unchanged

- Interest caps may be adjusted: Future governments could introduce stricter caps

- Write-off periods could extend (e.g., Plan 5 extended from 30 to 40 years)

Interest FAQ

When are interest rates adjusted each year?

If interest rates drop, will my monthly payments decrease?

How can I check my interest rate?

Could interest rates drop to 0%?

Further Reading

Why the "Expiry Date" is the most important factor for Plan 2 and Plan 5 loans.

A deep dive into when extra payments save you thousands—and when they are a waste.