UK Student Loan Overpayment Guide: When to Pay Extra and When Not To

Core conclusion: 85% of borrowers should NOT overpay. This article uses math to show why, and which high earners are the exception.

After receiving a bonus or inheritance, the instinct is "pay off my student loan." But UK income-contingent student loans aren't normal debt—they have a 30-year write-off period. For most people, overpaying is like throwing money into the sea.

Mental Accounting vs Mathematical Reality

Humans naturally hate debt, but student loans break traditional debt logic:

Psychological Appeal

- • "Debt-free" satisfaction

- • Reduces future interest

- • Simplifies finances

- • Removes uncertainty anxiety

Mathematical Truth

- • 85% of borrowers never clear principal

- • Money earns higher returns elsewhere

- • Monthly payments don't change (PAYE is income-based)

- • Overpayments = wasted if written off

Mathematical Validation: Who Should Overpay?

Overpayment only makes sense for those who "will clear the full debt before write-off".

Case 1: High Earner (Should Overpay)

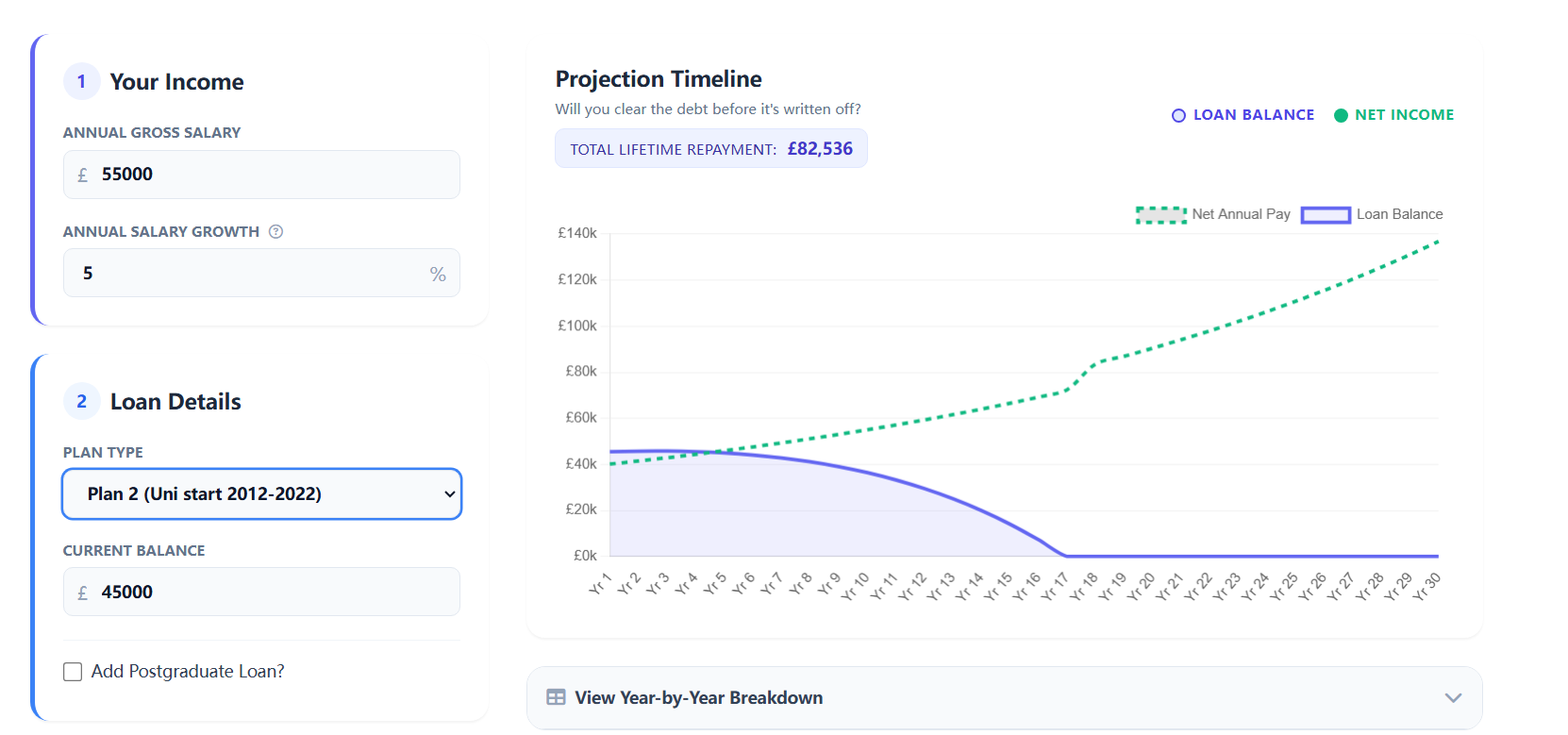

Profile: plan 2, £55,000 salary, 5% annual growth, £45,000 loan balance

• Calculator shows: Repaid in 17 years (13 years before write-off)

• Total repayment: £82,536 (£37,536 interest)

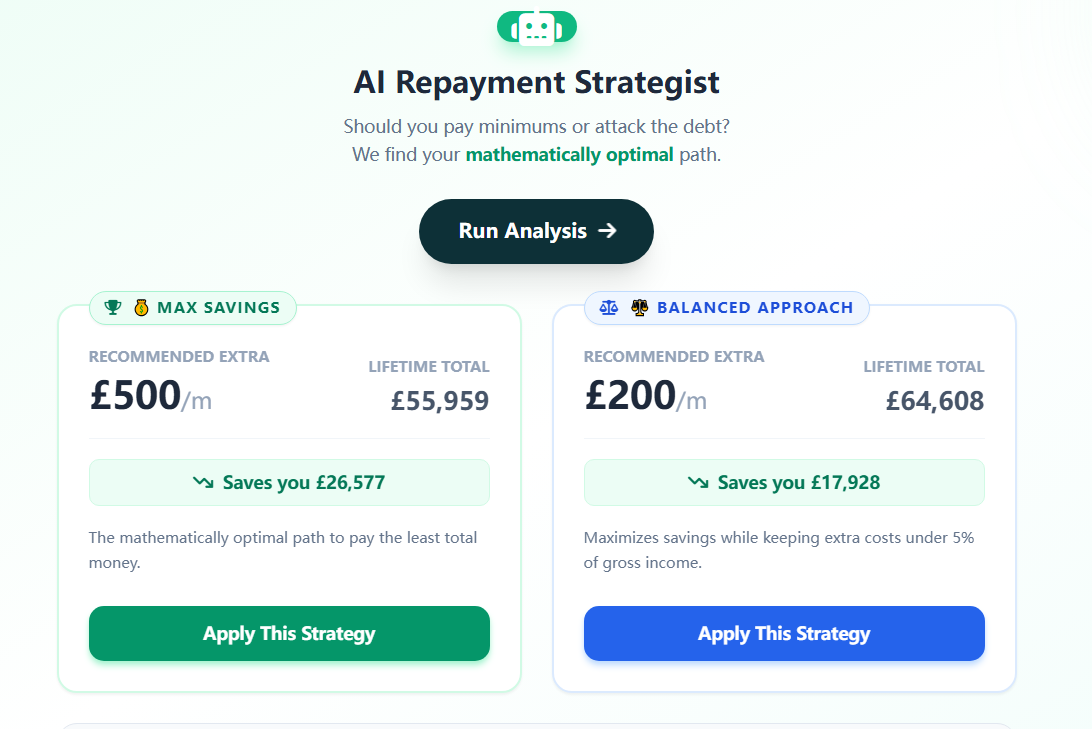

• If overpay £500/month: Repaid in 7 years, save £26,577 interest. And If overpay £200/month: Repaid in 11 years, save £17,928 interest

Conclusion: Overpayment makes sense, but only after building an emergency fund.

Case 2: Middle Earner (Should NOT Overpay)

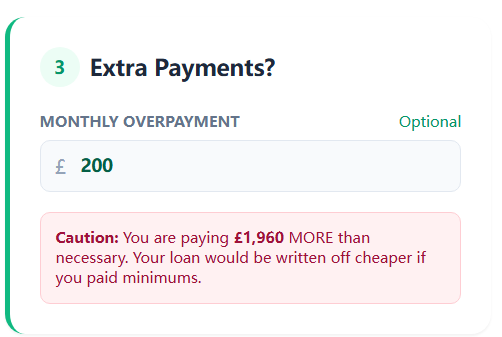

Profile: £38,000 salary, 3% annual growth, £50,000 loan balance

• Calculator shows: 30 years (write-off) → balance cancelled

• Total repayment: ~£83,368 (never clears principal)

• If overpay £200/month: Still 20 years to write-off, total £85,328

• Loss: £1,960

Conclusion: Money better used for house deposit or investments—overpayment is a loss.

Alternatives: Better Uses for Your Money

If you have extra cash, these almost always beat overpaying:

- Build Emergency Fund: 3-6 months expenses (£5,000-15,000) for job loss or emergencies

- LISA Savings: £4,000/year with 25% (£1,000) government bonus for first home

- Stocks & Shares ISA: Historical returns 7-10%, far exceeding student loan effective rates

- Pension Contributions: Employer matching = free money, plus tax relief

- Pay High-Interest Debt: Credit cards (20% APR), overdrafts (40% APR) are top priority

Hidden Risks of Overpayment

- Irreversible: Once paid, no refunds if you lose your job or income drops

- Loss of Liquidity: Money is locked away, unavailable for emergencies

- Opportunity Cost: Missed property gains, investment returns, and life experiences

- Policy Change Risk: Government could adjust write-off terms in future

When to NEVER Overpay

- • Earn under £45,000 with no rapid growth expected

- • No 3-month emergency fund

- • Have credit cards or higher-interest debt

- • Planning to buy property within 5 years (need deposit)

- • Career unstable or considering a change

Overpayment FAQ

Will overpayment reduce my monthly PAYE deductions?

Can I make partial overpayments?

If I inherit £30,000, should I clear my loan?

How do I know if I'm a high earner who should overpay?

Further Reading

Understanding interest calculation for decision-making

Why time is your best friend